Financing a custom home in Silicon Valley is fundamentally different from a standard mortgage. Buyers typically need a construction-to-permanent loan, a down payment of 20 to 30 percent, and a lender experienced with high-value projects. Understanding how draw schedules, appraisals, and interest rate locks work before you break ground can save you hundreds of thousands of dollars and prevent costly construction delays.

Silicon Valley land is among the most expensive in the country, and building a custom home here means navigating a financing process that most local banks aren't fully equipped to handle. The gap between a $200,000 tract home mortgage and a $4 million custom construction loan isn't just about size. The structure, the risk management, and the lender requirements are entirely different. Buyers who walk in unprepared often face delays, budget overruns, or loan denials that could have been avoided with the right guidance upfront.

Key Takeaways

- Construction-to-permanent loans are the standard financing vehicle for custom builds in Silicon Valley, converting to a traditional mortgage once the home is complete.

- Expect a down payment of 20 to 30 percent of the total project cost, which includes both land and construction expenses.

- Lenders release funds in draws tied to construction milestones, not in a lump sum, so cash flow planning is critical throughout the build.

- Appraisals for custom homes are based on projected value, not comparable sales, which creates risk if the finished home doesn't appraise to cost.

- Interest rate locks on construction loans are typically shorter than on standard mortgages and require careful timing to protect your budget.

- Working with a builder like Supple Homes INC who understands the local financing landscape can smooth the process significantly.

How Is Custom Home Financing Different from a Standard Mortgage?

When you buy an existing home, a lender can assess its value based on what similar homes nearby have sold for. That's straightforward. When you're building from scratch, there is no finished home to appraise. The lender is essentially funding a project, not a property, which changes everything about how the loan is structured.

Construction loans are short-term instruments, typically 12 to 18 months, designed to fund the build phase. Once construction is complete, the loan either converts to a permanent mortgage or the borrower refinances into one. This two-phase structure means buyers in Silicon Valley are navigating two underwriting processes, sometimes with two different lenders, for a single home.

Construction-to-permanent loans, also called one-time close loans, combine both phases into a single closing event. This eliminates a second round of closing costs and protects buyers from the risk that lending conditions worsen between the construction phase and the permanent mortgage phase. In high-cost markets like Silicon Valley, where closing costs on a $3 to $5 million loan can run into the tens of thousands of dollars, a one-time close structure offers real financial protection.

What Loan Types Are Available for High-End Custom Builds?

Not every lender offers construction loans for luxury projects, and the ones that do often have very different terms. Here's how the main options compare for Silicon Valley buyers.

Given that most Silicon Valley custom homes exceed the conforming loan limit by a wide margin, jumbo construction loans are the most common route. These require excellent credit, typically 720 or above, significant liquid reserves, and a detailed builder contract before the lender will even issue a pre-approval.

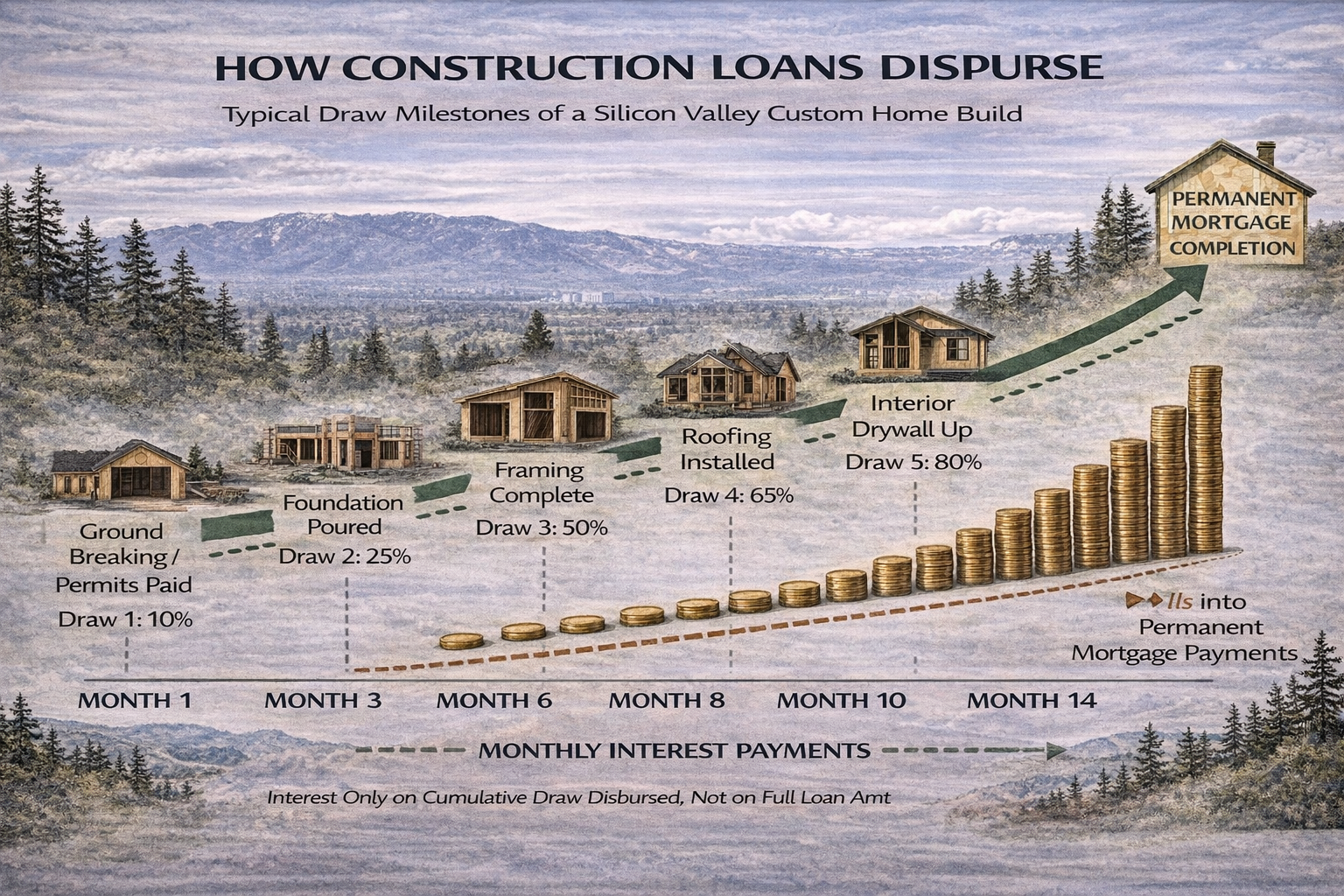

What Does the Draw Schedule Actually Mean for Your Budget?

One of the most misunderstood aspects of construction financing is how money actually moves during the build. Unlike a purchase mortgage where funds are released at closing, construction lenders disburse money in stages called draws. Each draw corresponds to a completed milestone, such as foundation poured, framing complete, or roofing installed.

Most lenders require an independent inspection before each draw is released. In Silicon Valley, where inspectors and bank representatives are often backlogged, delays between milestone completion and draw disbursement can stretch from a few days to several weeks. This means your builder needs adequate cash reserves to continue working while they wait for the next draw, and buyers should discuss this explicitly in the builder contract before signing anything.

During the draw period, you pay interest only on the funds that have been disbursed, not on the full loan amount. That's good news for cash flow, but it also means your monthly obligation increases with each draw. Buyers should model this out across the full construction timeline so the rising interest payments don't catch them off guard.

Step-by-Step: How to Finance a Custom Home Build in Silicon Valley

- Assess your full project budget. Land acquisition, design fees, permits, construction, and carrying costs must all be factored in before approaching a lender. In Silicon Valley, permits alone can add 5 to 10 percent to total project costs.

- Select a lender with jumbo construction loan experience. Not all banks offer these products. Look for private banks, regional lenders, or specialty mortgage companies with a track record in the Bay Area luxury market.

- Get pre-approved before finalizing your builder contract. Lenders will want to review your builder's license, insurance, and financial standing. Having a pre-approval in hand also gives you leverage in negotiations with your builder.

- Lock in your rate strategically. Discuss extended rate lock options with your lender. Some construction-to-permanent products offer locks up to 24 months, which is worth the premium in a volatile rate environment.

- Understand the appraisal process. Your lender will order an "as-completed" appraisal based on architectural plans and local comps. Review the appraisal assumptions carefully before you close.

- Establish a contingency reserve. Keep 10 to 15 percent of total construction cost in liquid reserves outside of your down payment. Silicon Valley builds routinely encounter cost increases from material pricing shifts or subcontractor delays.

- Monitor draw disbursements actively. Don't assume your lender's inspection schedule matches your builder's timeline. Stay involved in the draw process to avoid gaps that stall construction.

How Much Do You Actually Need for a Down Payment?

For jumbo construction loans in California, most lenders require a minimum down payment of 20 to 25 percent of the total project cost, which includes both land and construction. Some lenders servicing Silicon Valley's luxury tier push that figure to 30 percent for projects exceeding $5 million. On a $4 million build, that's a minimum of $800,000 to $1 million in equity required before the first nail is driven.

If you already own the land outright, that equity typically counts toward your down payment requirement. This is a significant advantage for buyers who purchased a lot separately and are now ready to build. A Silicon Valley homeowners guide can help you think through whether buying land first makes financial sense for your situation.

Buyers using funds from stock sales, RSU vesting, or business distributions should be prepared to document the source of those funds thoroughly. Lenders in this space are required to verify that down payment funds haven't been borrowed, and tech-sector income with variable components requires additional documentation.

What Are the Biggest Financial Mistakes Custom Home Buyers Make?

- Underestimating total project cost. The builder contract price rarely reflects the final cost. Change orders, upgraded finishes, and permit delays routinely push Silicon Valley custom builds 10 to 20 percent over initial estimates.

- Choosing a lender based on rate alone. A lender who offers a quarter-point lower rate but has no experience with custom construction draws or luxury appraisals can cost you far more in delays and complications.

- Skipping the contingency reserve. Treating your loan amount as your total budget with nothing held in reserve is one of the most common and painful mistakes in custom construction.

- Not understanding the appraisal gap risk. If your as-completed appraisal comes in below the cost to build, you'll need to cover that gap in cash. Many buyers don't plan for this scenario.

- Assuming the builder's preferred lender is the best option. Some builders receive referral incentives. Always get at least two competing loan quotes before committing.

- Neglecting to account for interest carry costs. Interest payments during the 12 to 18-month build phase aren't small. On a $3 million construction loan, even at a moderate rate, you could pay $150,000 or more in interest before the home is finished.

Working with a custom house builder in Silicon Valley who has navigated these challenges repeatedly is one of the best protections a buyer can have against these pitfalls.

Does Building in Silicon Valley Still Make Financial Sense?

It's a fair question, especially when land costs are steep and construction timelines are long. But many buyers who've explored the market in depth find that building custom isn't just a lifestyle choice. It's increasingly a financial one too. Understanding why build custom home in this market reveals advantages that resale properties simply can't offer.

Custom homes in premium Silicon Valley zip codes including Los Altos Hills, Atherton, Saratoga, and Monte Sereno have consistently commanded price premiums of 15 to 30 percent above comparable resale inventory, largely because of their newer systems, energy efficiency, and technology integration. Buyers who build with efficiency-focused designs can also reduce long-term operating costs significantly compared to older inventory in the same neighborhoods.

The financing burden is real, but so is the asset. A well-planned custom home in this region tends to hold value exceptionally well, and the ability to design exactly what you need from the ground up, including home offices, multigenerational suites, and smart infrastructure, means you're less likely to outgrow or resell prematurely. Thoughtfully designing spaces that match your household's actual needs is something a resale home rarely delivers.

Nearby Areas Where Supple Homes INC Supports Custom Builds

Silicon Valley's custom home market spans a wide geography. Supple Homes INC works with buyers across the region, including in Los Altos Hills, Atherton, Saratoga, Los Gatos, Monte Sereno, Palo Alto, Menlo Park, Cupertino, and the surrounding communities. Each city has its own permitting timeline, lot requirements, and ADU regulations that directly affect financing structures and project scope. Local expertise in these markets is not optional. It's essential.

If you're exploring home remodeling in Silicon Valley as an alternative to new construction, the financing options and timelines look quite different, and that comparison is worth understanding before committing to either path.

Frequently Asked Questions

What type of loan is needed for a custom build?

Most buyers use a construction-to-permanent loan, also called a one-time close loan. This product funds the build phase as a short-term construction loan, then automatically converts to a standard mortgage once the home is complete and the certificate of occupancy is issued. For luxury projects in Silicon Valley, this will typically be structured as a jumbo construction loan, as project costs nearly always exceed conforming loan limits.

How much down payment is required for luxury construction?

For jumbo construction loans in California, expect lenders to require 20 to 30 percent of the total project cost as a down payment. That includes both land and construction expenses. If you already own the land free and clear, that equity generally counts toward the required down payment, which can significantly reduce the cash you need to bring to the table at closing.

Should I use the builder's preferred lender?

Not necessarily. Builders often have preferred lender relationships that may or may not be in your best financial interest. Always get at least two competing loan quotes before committing. That said, a lender who has worked closely with your builder before does have a practical advantage in understanding how that builder structures draw requests and manages the construction timeline, so the relationship has some value beyond just rate.

How can I protect my budget against rising interest rates?

The most direct protection is an extended rate lock on a construction-to-permanent loan. Some lenders offer locks of 18 to 24 months, covering the full build period plus the conversion. These extended locks typically cost a small upfront premium, but in a volatile rate environment, locking in today's rate for a build that won't be complete for 14 to 18 months can be worth a meaningful premium. Talk to your lender about this option before you close on the construction loan.

What if my home doesn't appraise for the construction cost?

This is called an appraisal gap, and it's a real risk in a market where custom design choices and high-specification finishes don't always translate directly into appraised value. If your as-completed appraisal comes in below construction cost, your lender will base the loan on the lower appraised value, and you'll need to cover the difference in cash. The best protection is a conservative budget, a thorough review of the appraisal assumptions before closing, and maintaining a cash reserve specifically for this scenario.

Final Thoughts: Get the Financing Right Before You Break Ground

The financing structure you choose for a custom home in Silicon Valley will shape every phase of your project, from how much flexibility you have with design changes to how exposed you are when interest rates shift or a subcontractor causes delays. Getting this right at the start isn't just good financial planning. It's how experienced buyers protect a project that may take 18 months and several million dollars to complete.

The best outcomes in custom construction happen when buyers, builders, and lenders are aligned from the very beginning. That's the approach Supple Homes INC brings to every project across Silicon Valley. If you're ready to explore what building a custom home might look like for your situation, their team can walk you through the process, the financing considerations, and what to expect at each stage of the build.

Reach out to Supple Homes INC directly at (650) 649-4480 to start the conversation before you commit to a lender or sign a builder contract. The earlier you bring in the right team, the more options you'll have.